Understanding who qualifies for Obamacare is essential for families and individuals seeking affordable health insurance. This blog post will provide an in-depth look into the ACA, which has revolutionized healthcare coverage for families and individuals seeking affordable health insurance, including guaranteed issue provisions that ensure coverage to all applicants regardless of pre-existing conditions and medical loss ratio requirements mandating insurers to spend a certain percentage of premium revenue on actual medical care.

We’ll explore employer-sponsored plans under Obamacare, focusing on minimum value standards set forth by the ACA as well as capped out-of-pocket expenses according to federal guidelines. Furthermore, we delve into how individual mandate penalties were eliminated under the Inflation Reduction Act.

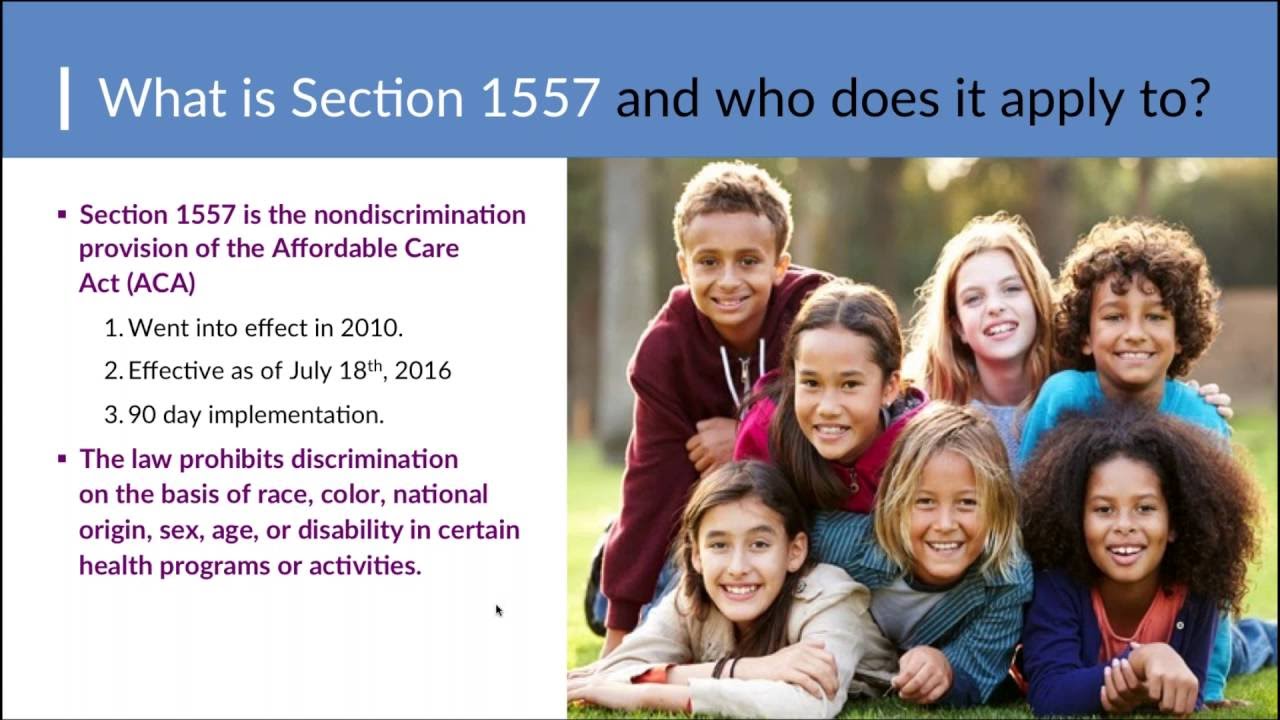

In addition to these topics, we cover Section 1557’s discrimination prohibition measures which ensure equal access to health insurance without bias based on race, color, national origin, sex, age, or disability status.

Table of Contents

- Who Qualifies for Obamacare?

- The Impact of Obamacare on Healthcare Coverage

- Guaranteed Issue Provisions Providing Coverage to All Applicants

- Medical Loss Ratio Requirements Ensuring Insurers Spend Premium Revenue on Medical Care

- Freedom from Job Lock with ACA

- Employer-Sponsored Plans Under Obama Care

- Elimination of Individual Mandate Penalties

- Section 1557 and Discrimination Prohibition

- Conclusion

Who Qualifies for Obamacare?

The Affordable Care Act, also known as Obamacare, provides health insurance to millions of Americans. If you are considering buying health insurance or want to know if you qualify for coverage under the ACA, read on.

Open Enrollment

If you do not have health coverage through your employer or a government program like Medicare or Medicaid, then you can buy individual coverage during open enrollment periods. Open enrollment typically runs from November 1st to January 15th each year but may vary depending on your state. During this time frame, anyone who meets the eligibility requirements can enroll in an ACA plan.

Expanded Medicaid

The ACA expanded Medicaid eligibility so that more low-income individuals and families could access affordable healthcare. Each state has different income limits and other criteria that determine whether someone is eligible for Medicaid under the expansion rules.

Immigration Status

To be eligible for Marketplace coverage through the ACA, immigrants must be lawfully present in the United States. This includes green card holders (permanent residents), refugees/asylum seekers with legal status, and others who meet certain immigration statuses defined by federal regulations.

The Impact of Obamacare on Healthcare Coverage

Since its enactment in 2010, the Affordable Care Act (ACA), also known as Obamacare, has significantly expanded healthcare coverage for millions of Americans. Key provisions such as guaranteed issue regulations and Medical Loss Ratio requirements have ensured comprehensive health insurance options are available regardless of pre-existing conditions or health status.

Guaranteed Issue Provisions Providing Coverage to All Applicants

The ACA includes a guaranteed issue provision, which requires insurers to offer health coverage to all applicants, regardless of their medical history or current health status. This means that individuals with pre-existing conditions can no longer be denied coverage or charged higher premiums based solely on their health.

Medical Loss Ratio Requirements Ensuring Insurers Spend Premium Revenue on Medical Care

In addition to guaranteed issue provisions, the ACA also established Medical Loss Ratio (MLR) requirements. These mandate that insurers spend at least 80% of premium revenue on medical care and quality improvement activities while limiting administrative costs and profits. The MLR ensures those who qualify for Obamacare receive value for their premium dollars by requiring insurance companies to invest more in actual healthcare services rather than overhead expenses.

The Impact of Obamacare on Healthcare Coverage has been significant in providing coverage to all applicants and ensuring that premium revenue is spent on medical care. Additionally, the ACA has provided increased opportunities for self-employment and entrepreneurship through accessible marketplace plans.

Freedom from Job Lock with ACA

One notable benefit provided by the Affordable Care Act (ACA), or Obamacare, is freeing individuals from “job lock,” allowing them more flexibility in pursuing self-employment and entrepreneurship without fear of losing their health insurance. Prior to Obamacare, many workers were hesitant to leave their jobs due to concerns about maintaining healthcare coverage. However, under the new regulations, they can access affordable options through state-based marketplaces or federal exchanges.

Increased Opportunities for Self-Employment and Entrepreneurship

The elimination of job lock has led to a surge in entrepreneurial activity as people are no longer tied down by employer-sponsored health insurance. With increased freedom and opportunities for self-employment, individuals can now pursue their passions while still having access to quality healthcare coverage. This change promotes economic growth and innovation within various industries.

Accessible Marketplace Plans Through State-Based Marketplaces or Federal Exchanges

- State-based marketplaces: Some states have established their own online platforms where residents can shop for qualified health insurance that meet ACA requirements.

- Federal exchanges: In states that did not establish a marketplace, residents can use the federally facilitated exchange at HealthCare.gov during open enrollment periods to buy health insurance that meets all necessary guidelines set forth by the law.

The ACA has enabled individuals to gain freedom from job lock and pursue self-employment or entrepreneurship opportunities, providing more flexibility in the labor market. Employers must now satisfy certain minimum value criteria as stipulated by the ACA and also have limits on their out-of-pocket costs set in accordance with federal directives.

Employer-Sponsored Plans Under Obama Care

The Affordable Care Act (ACA), also known as Obamacare, has established certain requirements for employer-sponsored health insurance. Large employers are mandated to offer their employees a plan that covers at least 60% of expected healthcare costs while capping out-of-pocket expenses according to federal guidelines. This ensures minimum value standards are met for employer-sponsored plans, allowing families more flexibility when choosing career paths without sacrificing healthcare security.

Minimum Value Standards Set Forth by the ACA

In order to comply with the ACA, large employers must provide a health insurance plan that meets specific minimum value standards. These standards require that the plan cover at least 60% of total allowed costs and include substantial coverage for inpatient hospitalization and physician services. By setting these benchmarks, the ACA aims to ensure comprehensive health coverage is available through employer-sponsored plans.

Capped Out-of-Pocket Expenses According to Federal Guidelines

To further protect consumers from excessive medical expenses, the ACA imposes limits on out-of-pocket costs for individuals enrolled in an approved health insurance plan. The maximum allowable amount varies depending on factors such as family size and income level but generally follows annual inflation adjustments set forth by the Inflation Reduction Act. By capping these expenses, families can have greater peace of mind knowing they will not face insurmountable financial burdens due to unforeseen medical events.

Employer-sponsored plans under Obama Care offer individuals and families the ability to obtain quality health care coverage at an economical rate. Furthermore, eliminating individual mandate penalties allows people greater freedom of choice when selecting qualified health insurance that meets their needs.

Elimination of Individual Mandate Penalties

After December 31st, 2018, the Affordable Care Act (ACA) underwent a significant change with the elimination of individual mandate penalties. Those who opt out of approved health insurance will no longer be subject to financial penalties. By removing these penalties, individuals are granted greater freedom in deciding whether obtaining health insurance is right for them.

The elimination of individual mandate penalties has provided individuals with more flexibility when it comes to obtaining healthcare coverage. Moving on, Section 1557 and Discrimination Prohibition ensures equal access to health plans without discrimination for all eligible citizens.

Section 1557 and Discrimination Prohibition

The ACA has taken positive steps to ensure that all individuals who qualify for Obamacare, regardless of gender identity or sexual orientation, have equal access to healthcare by introducing Section 1557. This ensures that all individuals, regardless of their personal identification/preferences within this spectrum, have equal access to comprehensive health coverage.

- Equal access to health plans without discrimination: Under Section 1557, insurance companies are required to provide coverage options without discriminating against applicants based on their gender identity or sexual orientation. This means that transgender individuals, for example, cannot be denied coverage or charged higher premiums solely because of their gender identity.

- Inclusivity and fairness in healthcare coverage: By prohibiting discriminatory practices in the provision of health insurance, Section 1557 promotes a more inclusive environment where everyone can obtain the care they need without fear of prejudice or bias. This not only benefits those directly affected by these protections but also contributes to a healthier society overall.

To further support these provisions, the ACA also includes preventive services guidelines that require most private insurers to cover essential preventive services – such as cancer screenings and vaccinations – at no cost-sharing measures like copayments or deductibles. These guidelines apply equally across all genders and orientations – ensuring every individual has access to vital preventative care regardless of their background.

In essence, Section 1557 plays an integral role in fostering equality within our nation’s healthcare landscape by guaranteeing fair treatment for all Americans who qualify for Obamacare, regardless of their gender identity or sexual orientation.

Conclusion

Those who qualify for Obamacare are individuals who are lawfully present in the United States and can buy health insurance through the ACA’s Health Insurance Marketplace. It’s important to note that immigration status does not affect eligibility for emergency medical care, however, undocumented immigrants are not eligible to buy health coverage through the Marketplace or qualify for Medicaid. If you have pre-existing conditions, insurers cannot deny you coverage or charge you more because of your health status.

Overall, the ACA has made significant strides in improving health coverage and access to care for millions of Americans.