When it comes to understanding how does Obama Care work, there’s a lot more to it than meets the eye. The ACA, otherwise known as Obama Care, was made to give accessible health coverage choices to numerous Americans who were without insurance or had high expenses. In this blog post, we’ll delve into the complexities of how does Obama Care work and its effects on healthcare in America.

We’ll explore key components of the ACA, such as state-based marketplaces and premium tax credits that help make health insurance more accessible for many families. You’ll learn about various types of plans available under Obama Care and the factors affecting premium costs. Additionally, we will discuss open enrollment periods and special circumstances that allow individuals to enroll outside regular timelines.

Furthermore, you can expect an analysis of recent changes brought by the American Rescue Plan Act and their implications on healthcare coverage.

This comprehensive overview aims to answer all your questions regarding how does Obama Care work so you can confidently navigate your way towards securing quality healthcare coverage tailored specifically to your needs.

Table of Contents

- Understanding the Affordable Care Act (ACA)

- Key Components of the ACA

- The Role of State-Based Marketplaces

- How Does Obama Care Work?

- Open Enrollment & Special Enrollment Periods

- American Rescue Plan Act’s Impact on Healthcare Coverage

- Conclusion

Understanding the Affordable Care Act (ACA)

The Affordable Care Act (ACA), also known as Obama Care, was enacted in 2010 to help low-income households obtain affordable health insurance and allow states to expand Medicaid coverage. This legislation established marketplaces where people can shop for various health insurance options tailored to their needs.

Key Components of the ACA

- Mandatory Coverage: The ACA requires most Americans to have some form of health insurance or face a tax penalty.

- Marketplace Exchanges: State-based online platforms were created for individuals and families who do not receive employer-sponsored coverage or qualify for government programs like Medicare or Medicaid.

- Premium Subsidies: Financial assistance is available through premium tax credits based on income level, making it more affordable for eligible individuals and families to purchase private plans on marketplace exchanges.

- No Pre-existing Condition Discrimination: Insurance companies are prohibited from denying coverage or charging higher premiums due to pre-existing conditions under the ACA.

The Role of State-Based Marketplaces

State-run exchanges, either alone or with the federal government’s help, offer an array of qualified health plans from various insurers that meet state and federal guidelines. State-run marketplaces provide a variety of health plans from various insurance providers that adhere to both state and federal guidelines.

Consumers can compare plan options side-by-side using an easy-to-understand format designed specifically for this purpose – ultimately allowing them greater control over selecting policies best suited towards meeting unique individualized needs while still remaining within budgetary constraints imposed upon them throughout daily life experiences encountered by all Americans today.

The ACA has revolutionized the healthcare system in America, introducing an intricate and multifaceted law. Health Insurance Options Under Obama Care offer individuals and families more options for coverage, including different types of plans with varying premium costs based on individual circumstances.

How Does Obama Care Work?

If you’re looking for health insurance coverage, the Affordable Care Act (ACA), also known as Obama Care, offers different options depending on your income level and chosen plan. The ACA prohibits lifetime monetary caps and allows parents to keep their children on their policies until age 26.

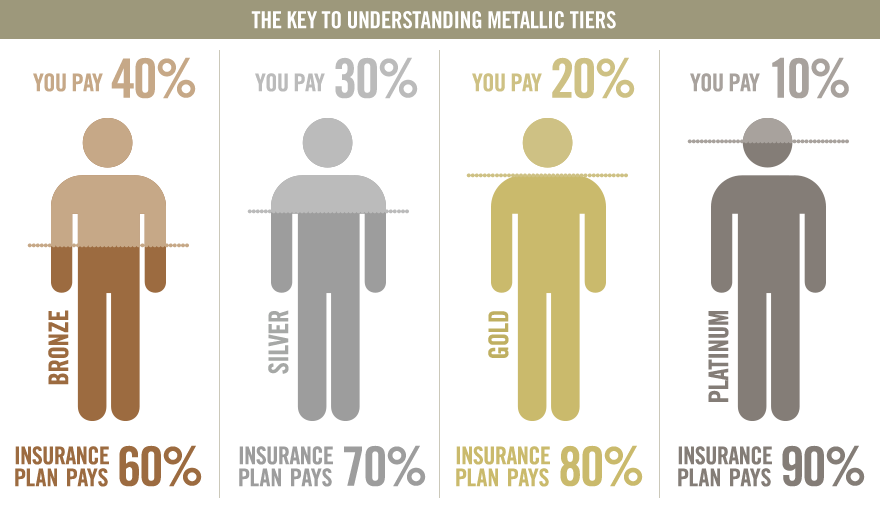

Types of Plans Available Under Obama Care

There are four primary types of health insurance plans available under Obama Care: Bronze, Silver, Gold, and Platinum. These plans offer varying levels of coverage and corresponding monthly premium rates:

- Bronze – lowest monthly premium but highest out-of-pocket costs when receiving care.

- Silver – moderate monthly premium with lower out-of-pocket expenses than Bronze.

- Gold – a higher monthly premium but lower out-of-pocket costs compared to Silver.

- Platinum – the highest monthly premium offering the least amount in terms of cost-sharing.

Factors Affecting Premium Costs

Premiums vary based on several factors such as location, age, tobacco use, individual vs family enrollment status, and whether an applicant qualifies for financial assistance like tax credits. The ACA also prohibits insurance companies from charging higher premiums due to pre-existing conditions or gender-based pricing differences. Comparing multiple options within your state’s marketplace can help you find a suitable plan that meets both your healthcare needs and budget constraints.

Health insurance options under Obama Care have given individuals and families more control over their health care coverage. Let’s now examine the tax credits and monetary aid that can assist in making these plans more economical.

Premium Tax Credits & Financial Assistance

Another example of “How does Obama Care work” is by providing financial assistance in the form of premium tax credits to help eligible families and individuals afford health insurance through the marketplace. These tax credits can significantly reduce monthly premium costs, making comprehensive healthcare coverage more accessible for low-income households.

How Premium Tax Credits Work

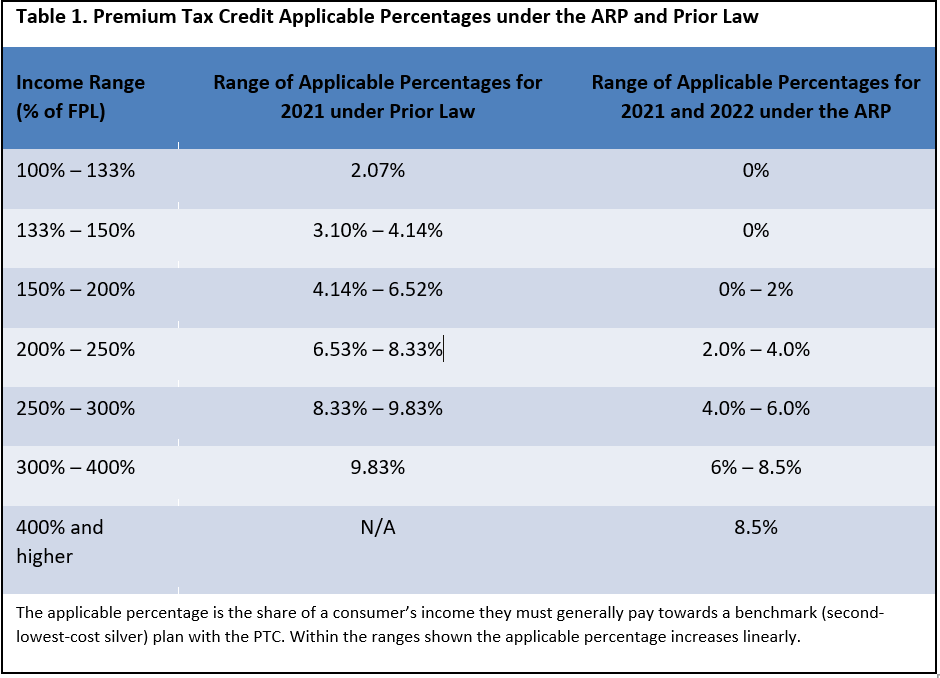

Premium tax credits are determined by various elements, including income level, locality, and the price of plans available in a particular region. To qualify for these credits, your household income must fall between 100% and 400% of the federal poverty level (FPL).

The amount of the credit increases as your income falls within this range. If you have access to affordable employer-sponsored insurance or are eligible for government programs like Medicaid or Medicare, premium tax credits cannot be received.

Additional Assistance Programs Like Medicaid or CHIP

- Medicaid: A state-federal partnership program providing health coverage for low-income Americans who meet eligibility requirements.

- Children’s Health Insurance Program (CHIP): A separate but related program offering affordable health insurance specifically designed for children under age 19 whose families don’t qualify for Medicaid but still need financial assistance with healthcare costs.

To determine whether you’re eligible for any of these programs or premium tax credits, visit the Health Insurance Marketplace and complete the eligibility screener.

Premium tax credits and fiscal support can assist in making health insurance more cost-effective for those eligible. To learn more about open enrollment periods and special enrollment triggers, continue reading below.

Open Enrollment & Special Enrollment Periods

The process of obtaining health insurance through the Affordable Care Act is primarily done during the open enrollment period. This window typically begins on November 1st and ends on January 15th in most states, providing ample time for families and individuals to explore their options and select a suitable plan.

Navigating Open Enrollment Timelines

It is essential to be cognizant of the open enrollment time limits in order to evade forfeiting coverage. During open enrollment, consumers can take advantage of the legal requirement for insurance companies to offer plans and make informed decisions about their healthcare needs. If you miss the deadline, you may have limited opportunities to obtain coverage until the next open enrollment period.

Qualifying Events Triggering Special Enrollment Periods

- Losing job-based coverage: Within sixty days of losing job-based coverage, you can apply for Obama Care due to a qualifying event such as marriage, divorce, childbirth, or adoption.

- Marriage or divorce: A change in marital status allows both partners a special enrollment opportunity.

- Childbirth or adoption: Adding a new family member grants access to a special enrollment period as well.

- Moving residences: Relocating outside your current plan’s service area qualifies you for a special enrollment opportunity if other marketplace plans are available in your new location.

Open enrollment and special enrollment periods are important for understanding the different ways to obtain Obama Care insurance. The American Rescue Plan Act has had a significant impact on healthcare coverage, providing increased subsidies and COBRA extension benefits that can help those in need of health insurance.

American Rescue Plan Act’s Impact on Healthcare Coverage

The American Rescue Plan Act signed into law by President Joe Biden aims to provide additional support to ensure accessible healthcare services amidst ongoing challenges posed by the COVID-19 pandemic. This legislation includes increasing subsidies for Obama Care plans and extending COBRA regulations’ coverage periods, making it easier for families and individuals to obtain affordable health insurance.

Increased Subsidies Explained

Under the American Rescue Plan, eligible enrollees in the Health Insurance Marketplace can receive increased premium tax credits, lowering their monthly premiums. The new provisions ensure that no household will pay more than 8.27% of their income on a benchmark plan through the marketplace.

Additionally, those earning up to 150% of the federal poverty level may qualify for $0 premium plans with low out-of-pocket costs. These enhanced subsidies are available during both open enrollment and special enrollment periods until December 31st, 2023.

COBRA Extensions Benefits

The COBRA Act enables individuals who have lost job-based health insurance to temporarily maintain their coverage under certain conditions. Under the American Rescue Plan, individuals eligible for COBRA continuation coverage between April 1st and September 30th, 2023, can receive a temporary subsidy covering 100% of their COBRA premiums during this period – making it significantly more affordable for people experiencing job loss or reduced hours due to pandemic-related factors.

Conclusion

When it comes to how does Obama Care work, it has helped low-income households obtain affordable health insurance and allows states to expand Medicaid coverage by creating affordable tiered plans depending on your needs and financial capabilities. It also provides financial assistance in the form of premium tax credits to help eligible families and individuals afford health insurance through the marketplace. Finally, the American Rescue Plan Act has increased subsidies available for those who qualify and extended COBRA benefits making healthcare more accessible to families and individuals.