Importance of Consulting Licensed Agents When Considering Available Options

To gain insight into local regulations and discover the ideal coverage option for you, it is essential to consult with a certified representative who can provide direction on accessible policies in your area. This ensures that you are well-informed about any potential limitations or exclusions before committing to a plan.Get the right coverage for your needs. Consult with a licensed agent to navigate state-specific regulations on short-term health insurance. #Obamacare #HealthInsuranceCoverage Click to Tweet

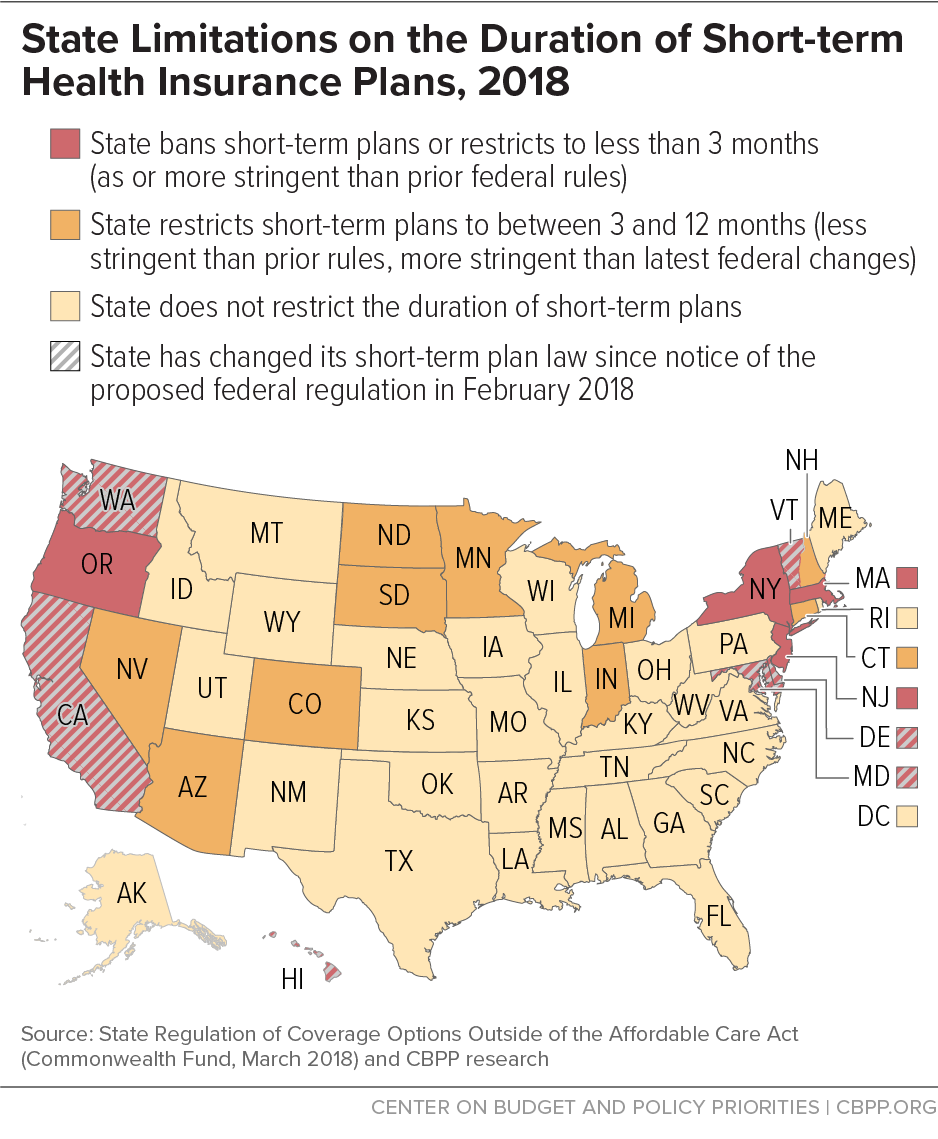

Consumer Disclosures and Limitations

The National Association of Insurance Commissioners (NAIC) adopted the Supplementary and Short-Term Health Insurance Minimum Standards Model Act in 1974, which was revised in 2023 to include provisions concerning short-term health plans. These revisions emphasize requirements for consumer disclosures, ensuring that individuals are aware of any limitations associated with their chosen policies.NAIC’s Role in Regulating Short-Term Health Insurance

The NAIC plays a crucial role in setting standards for state insurance regulators to follow when overseeing short-term health insurance plans. By updating the model act, they help ensure consumers have access to transparent information about their coverage options.Emphasis on Consumer Disclosure Requirements

- Mandatory disclosure: Insurers must provide clear explanations of policy terms and conditions, including exclusions or limitations related to pre-existing conditions and essential health benefits.

- Risk awareness: Consumers should be informed about potential risks associated with choosing a short-term plan over traditional health insurance or ACA-compliant coverage.

- Contact information: Insurers must supply contact details for further assistance regarding policy inquiries or filing medical claims.

Get informed about your short-term health insurance coverage. The NAIC ensures consumer disclosures and limitations are transparent. #ObamaCare #HealthInsurance Click to Tweet

Coverage Details and Family Options

Most short-term health insurance plans cover at least one doctor’s checkup at a low cost. However, payments for doctors will vary by plan. Emergency hospital care is typically covered, but medical transportation may not be included. Services and durable medical equipment might also be covered depending on your specific policy.- Doctor visits: Coverage often includes a minimum of one visit per year.

- Emergency hospital care: Generally provided, though the extent varies between policies.

- Medical transportation exclusions: Ambulance services are frequently excluded from coverage.

Get the coverage you need with short-term health insurance. Doctor visits and emergency hospital care are usually covered, but check your policy for details. #Obamacare #healthinsurance Click to Tweet

Conclusion

What Does Short Term Health Insurance Cover? Short-term health insurance policies are designed to provide temporary coverage for individuals and families who need medical benefits for a limited period. They offer various services such as emergency care, prescription drug coverage, and outpatient mental health treatment availability, however, it is essential to understand the limitations of these policies and state-specific regulations before purchasing them. Consulting licensed agents can help you get accurate information about what your policy covers.Contact Fiorella Insurance today for your free health insurance quote.