How to Get a Care Card: Pre-qualification Process

The first step of how to get a care card is the pre-qualification process. You will need to provide some basic information about yourself like name, address, and social security number. Once submitted, you’ll receive an instant decision on whether or not you qualify for the medical credit card along with details of your approved limit.Services covered under the CareCredit program

- Dental: Routine checkups, cleanings, orthodontics (braces), root canal treatment, and more are covered under this category.

- Vision: Eye exams, glasses, contact lenses, and LASIK surgery are a few examples of vision-related expenses that can be financed using CareCredit cards.

- Dermatology: Cosmetic procedures like Botox injections, microdermabrasion, and tattoo removals come under this category in addition to treating skin conditions such as acne or eczema.

- Cosmetic Surgery: Breast augmentation, liposuction, and rhinoplasty (nose job) are among many other surgical procedures that could be paid off using this card.

- Other Services: CareCredit also covers expenses related to hearing care, veterinary services, and weight loss programs.

Key Takeaway: The CareCredit Card is a healthcare credit card accepted by over 225,000 healthcare and wellness providers. The pre-qualification process allows you to check your eligibility without affecting your credit score, covering services such as dental work, eye exams, dermatology treatments, and cosmetic surgeries.

Financing Options and Interest Rates

The CareCredit Card offers a variety of financing options to help you manage your medical expenses. These include promotional periods of 6, 12, 18, or 24 months with no interest on purchases totaling $200 or more. If the balance is not paid in full by the end of the promotional period, an APR of 26.99% will be applied to any remaining amount.Promotional Periods Offered by Care Credit

- 6-month plan: No interest if paid in full within six months for purchases over $200.

- 12-month plan: No interest if paid in full within twelve months for purchases over $200.

- 18-month plan: No interest if paid in full within eighteen months for purchases over $200.

- 24-month plan: No interest if paid in full within twenty-four months for purchases over $200.

The CareCredit Card is an excellent option for managing medical expenses that you can’t afford to pay upfront. With its various promotional periods and no annual fee, it’s a great way to finance your medical needs without breaking the bank. #CareCard #AffordableCareAct Click To Tweet

Understanding the monetary terms and rates provided by Care Credit is essential for making an educated selection. As such, it is also essential to be aware of any controversies surrounding the enrollment process for Care Cards.

Key Takeaway: The CareCredit Card offers financing options with promotional periods of 6, 12, 18, or 24 months with no interest on purchases over $200. However, if the balance is not paid in full by the end of this period, an APR of 26.99% will be applied. To avoid additional charges due to high-interest rates, calculate your minimum monthly payments and stick to them throughout your repayment term using online tools like a credit card payment calculator.

Controversies Surrounding Enrollment Process

In recent years, there have been some controversies when it comes to “how to get a care card”. Due to misleading information provided during sign-up procedures, CareCredit was ordered to refund $34.1 million to cardholders. This highlights the importance of thoroughly researching and understanding all terms associated with obtaining a medical credit card like CareCredit.Cases of Misleading Information

Some cases reported that consumers were not adequately informed about the interest rates or promotional periods when signing up for a CareCredit Card. As a result, many people ended up paying more than they initially expected due to high-interest charges on their balances after the promotional period had expired. In response, Synchrony Bank has taken steps to improve transparency by providing clearer disclosures and enhancing consumer protections.Importance of Understanding Terms Before Applying

When learning how to get a Care card, it is crucial for potential users to fully understand all aspects of applying for and using a CareCredit Card before committing:- Educate yourself: Research various financing options available in the healthcare industry such as Health Savings Accounts (HSAs), personal loans, or general-use credit cards which may provide lower interest rates or additional perks that can be beneficial in the long run.

- Read the fine print: Make sure you read through all terms and conditions associated with any financial product you’re considering – including fees, interest rate structures, and repayment plans. Take the time to understand all terms and conditions of a financial product you’re considering in order to make an informed decision and avoid potential surprises.

- Ask questions: If you’re unsure about any aspect of a financial product, don’t hesitate to ask for clarification from the provider or seek advice from a trusted professional such as your healthcare provider, insurance agent, or financial advisor. They can be of assistance in selecting the most suitable solution for your circumstances.

Key Takeaway: CareCredit cards have faced controversies due to misleading information during sign-up procedures, resulting in a $34.1 million refund to cardholders. To avoid falling into similar traps, potential users should educate themselves on various financing options available in the healthcare industry, read the fine print of any financial product they’re considering, and ask questions if unsure about any aspect of it.

Alternative Financial Solutions

Before solely relying on medical credit cards like CareCredit, it is essential to explore other financial alternatives that may provide lower interest rates or additional perks in the long run. These options include Health Savings Accounts (HSAs), personal loans, and general-use credit cards with balance transfer promotions.Advantages & Usage of Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) are tax-advantaged accounts designed for individuals with high-deductible health plans. Contributions to HSAs are tax-exempt, the earnings accumulate without taxation and any withdrawals used for certified medical outlays also avoid taxes.Personal Loan Benefits Compared to Medical Credit Cards

Personal loans typically offer fixed interest rates and repayment terms, making them easier to budget than variable-rate lines of credit. Additionally, some lenders offer personal loans specifically tailored towards medical expenses which may have more favorable terms compared to generic personal loans.

General-Use Credit Cards Offering Balance Transfer Promotions

General-Use Credit cards often offer introductory 0% APR periods, allowing you to pay off your balance without incurring interest charges during the promotional period. However, it is crucial to ensure that you can repay the entire balance before the end of this period; otherwise, you’ll face high-interest rates similar to those on medical credit cards.Alternative methods of financing can be a practical way to fund #healthcare costs without emptying one’s wallet. However, it is important to explore all of your options before committing to any one solution, including exploring potential payment #plans with #providers and looking into types of available financial aid. #CareCard #AffordableCareAct #Obamacare Click To Tweet

Remember that each financial solution has its pros and cons, so carefully weigh your options based on your unique situation and needs. By exploring these alternatives and comparing them against CareCredit or other medical credit cards, you can make an informed decision about which option will best help manage your healthcare expenses while minimizing potential long-term costs.

Key Takeaway: Before relying solely on medical credit cards like CareCredit, it’s important to explore other financial alternatives such as Health Savings Accounts (HSAs), personal loans, and general-use credit cards with balance transfer promotions. HSAs offer tax advantages while personal loans have fixed interest rates and repayment terms. General-use credit cards may be advantageous for short-term expenses if you can pay off the balance before the end of the 0% APR period.

Exploring Financial Aid and Payment Plans

If you have not exhausted other options to pay your medical bill, such as financial aid, it is essential to explore these avenues before committing solely to a CareCredit Card. In some cases, using this card may forfeit other repayment opportunities available through different channels.Types of Financial Aid for Healthcare Expenses

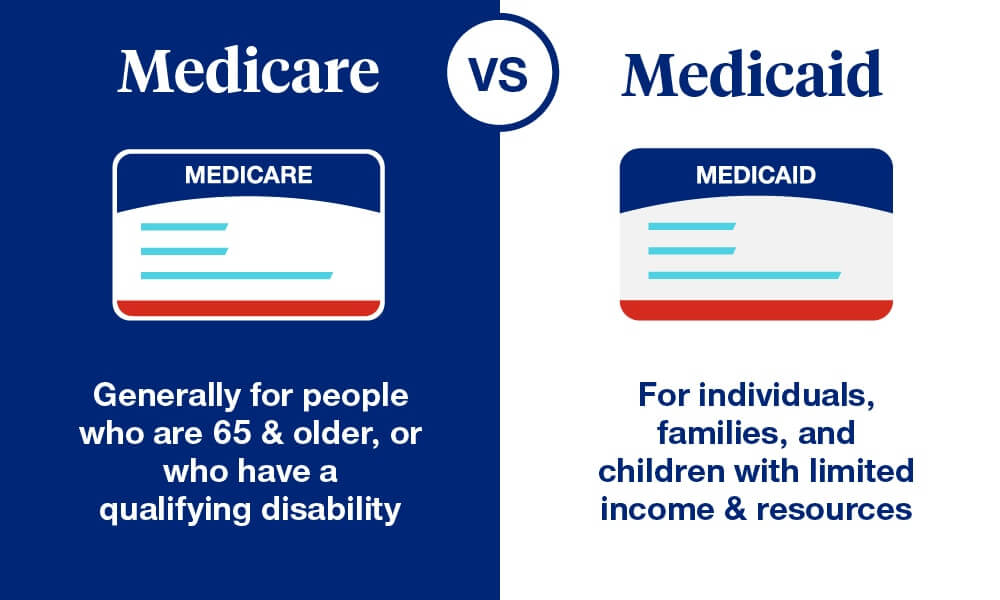

- Medicaid: A state and federal program that provides health coverage for low-income individuals and families. Eligibility varies by state.

- MEDICARE: A federal health insurance program primarily designed for people aged 65 or older but also covers certain younger individuals with disabilities.

- Hospital Charity Care Programs: Many hospitals offer charity care programs that provide financial assistance based on income levels. Contact your hospital’s billing department or social services office to inquire about eligibility requirements.

- Patient Assistance Programs (PAPs): Offered by pharmaceutical companies, PAPs help eligible patients receive prescription medications at little or no cost.

Discussing Payment Plans with Healthcare Providers

Before resorting to medical credit cards like CareCredit, consider discussing your financial situation with your healthcare provider. Many medical providers are open to negotiating payment plans or providing reduced rates for those unable to pay their bills in full. Taking advantage of available financial aid options and negotiating with healthcare providers can help alleviate the burden of high medical expenses without relying solely on a CareCredit Card. By exploring these alternatives, families and individuals will be better equipped in managing their healthcare costs effectively.Key Takeaway: Before getting a CareCredit Card for medical expenses, it’s important to explore financial aid options such as Medicaid and hospital charity care programs. By taking advantage of these alternatives, individuals can effectively manage their healthcare costs without solely relying on a credit card.

Conclusion

If you’re looking for a way to manage your healthcare expenses, obtaining a CareCredit Card can be an effective solution. Before applying, it’s important to understand the services covered and the prequalification process, financing options, and interest rates, as well as alternative financial solutions like HSAs or personal loans. Ultimately, evaluating personal needs in relation to healthcare financing options and communicating with health providers about potential payment plans can help you make informed decisions on how to get a care card.Contact Fiorella Insurance today for your free Obama Care Health Insurance Quote.