You know you need health insurance coverage, but you’re not sure exactly where to begin. Sound familiar? This is a common sentiment among Americans each year as they work to navigate the complexities of quality health insurance coverage for themselves and their families. One of the most frequent questions raised concerns the differences between Obamacare vs. Medicaid, and which program will be the right fit.

While both programs offer health insurance coverage to cover the costs of healthcare treatment, they are distinct from one another in a number of important ways. As you consider the health care insurance programs available to you from different insurance companies, remember, these medical care insurance programs involve different eligibility criteria, enrollment periods and cost-sharing schemes. Fortunately, between the two programs, there is a strong chance you will be able to find an affordable health insurance program that meets your healthcare needs from of the many private health insurance company’s participating in the exchanges.

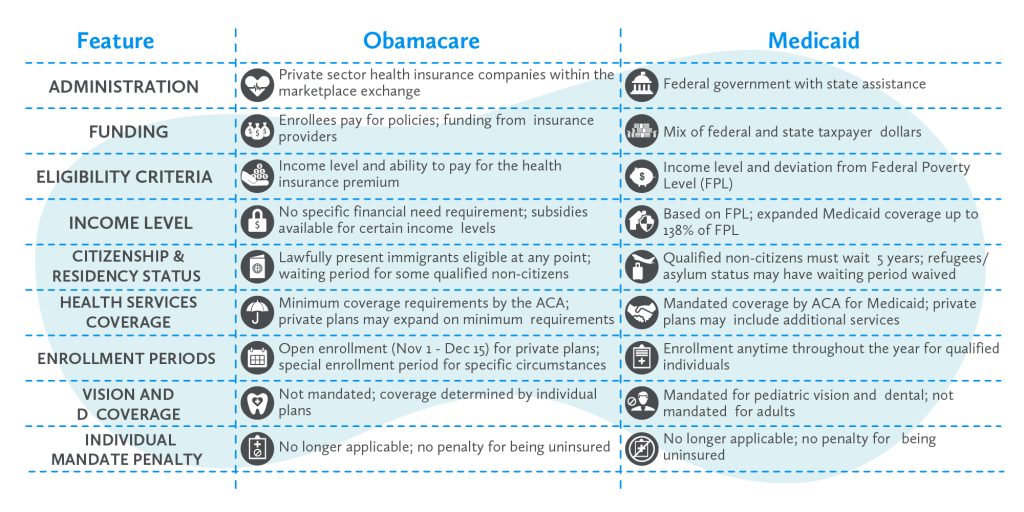

Administration of Obamacare vs. Medicaid

Perhaps the biggest difference between Obamacare and Medicaid is the entity responsible for administering the policies. Medicaid is administered by the federal government, with assistance from state-level offices. On the federal level, Medicaid is run by the Centers for Medicare and Medicaid Services (known as “CMS”). The program is funded by a mix of federal and state taxpayer dollars; however, each state runs its own Medicaid program entitlements differently resulting in varying degrees of coverage depending on the jurisdiction.

On the other hand, ACA plans under Obamacare are administered by private sector health insurance companies within the marketplace exchange. Enrollees are required to pay for their policies and funding for these policies is derived from the insurance provider itself. In some instances, discussed further below, the government may be able to offer subsidies for assistance with the cost of obama care health insurance coverage. However, these plans are considered completely distinct from government-run programs and are not funded by taxpayer dollars.

Eligibility requirements

Who Qualifies for Obamacare

Another important distinction between Obamacare vs. Medicaid concerns the criteria necessary to qualify for either program. Medicaid eligibility is determined based upon income level, and this program is reserved for those within a certain deviation of the federal poverty level. By contrast, Obamacare is freely available to anyone regardless of income – assuming the applicant is able to pay. The important eligibility criteria are as follows:

1. Income Level

The federal government provides eligibility guidelines for states to follow. In the background, the federal government pays a portion of the costs of Medicaid, while state tax revenue picks up the rest. An applicant for Medicaid must establish financial need, which is determined based on the applicant’s income and family size as compared with the Federal Poverty Line (“FPL”) – which is updated each year to address costs of living.

For instance, for a family of four, the FPL is set at $25,100 per year, so applicants earning this amount or less would qualify. In states with expanded Medicaid coverage, annual income up to 138 percent of FPL is considered financial need – so a family of four could earn up to \$34,368 annually and still qualify.

Obamacare plans do not have a financial need requirement to qualify, provided the applicant is able to make the regular payments necessary to afford the health care insurance premium. However, applicants earning up to 400 percent of FPL may be eligible for a subsidy to help with the costs of premiums. It is also important to note that applicants for an Obamacare plan who are also eligible for Medicare (based on age) must elect to take Medicare coverage as opposed to the private plan.

What is Medicare?

Medicare: Medicare is a program designed to help people over the age of 65, along with some younger individuals who have certain disabilities. While you may have to pay a premium, the main cost of your Medicare is paid for through your working years. Part of what is taken out of your paycheck each week now is what pays for your Medicare once you reach retirement age. Currently, Medicare benefits come in four parts.

- Part A: Hospital Care. This part pays for time spent in a medical facility.

- Part B: This part covers tests and procedures, meaning what happens to you while in the hospital or medical facility. Part B coverage requires a premium.

- Part C: Done as an alternative to normal Medicare coverage, Part C is known as Medicare Advantage plans, offer the benefits of Part A, B, and D, and are administered through private insurance companies.

- Part D: Part D covers prescription drug coverage. Part D is a required benefit of Medicare, unless you obtain it from a different source.

2. Citizenship & Residency Status

Anyone considered a “qualified non-citizen” must generally wait five years from the start of that status before being eligible for coverage by Medicaid. In some instances, applicants who are considered refugees or under asylum status may have this waiting period waived.

By contrast, a lawfully present immigrant may purchase coverage under an Obamacare plan at any point, regardless of when lawful presence status was achieved.

3. Health Services Coverage

In 2010, the Affordable Care Act was signed into law generating certain minimum requirements for coverage across any healthcare plan offered in the U.S. – including plans administered by Medicaid. From there, however, private plans under Obamacare may expand upon the minimum coverage requirements to include coverage for services including fertility treatment, cosmetic surgery, procedures determined to be “not medically necessary” or private rooms in a long-term care facility, to name just a few.

Also worth noting, states administering Medicaid plans are mandated to provide pediatric vision and dental coverage, whereas private Obamacare plans are not.

Enrollment Periods

One very important distinction between Obamacare versus Medicaid is the concept of “open enrollment,” which only applies to private healthcare plans under Obamacare. Open enrollment is a six-week period occurring from November 1st through December 15th during which new enrollees can sign up for a plan or current enrollees can make changes to the terms of their policy. By contrast, Medicaid enrollment can occur anytime throughout the year provided the enrollee qualifies under the income and residency requirements.

For the uninsured who do not qualify for Medicaid, a “special enrollment period” may be an option. As the name suggests, enrollment outside the open enrollment period may be possible if certain circumstances occur, including:

- Loss of coverage due to termination or resignation of employment

- Marriage or birth of a child

- Death of a primary policyholder

- Significant change in income

Under current laws, according to the supreme court, anyone who is uninsured will no longer face the individual mandate taxation for not having healthcare coverage, so missing the open enrollment period will not result in a penalty.

At Fiorella Insurance, we are pleased to work with individuals and families seeking affordable health insurance coverage. Please give us a call today! Or start application using the form below.